LFTL: Uncovering Hidden Costs

Every restaurant owner knows the big-ticket costs: rent, food, labor, labor, and labor.

But in our work managing the books for restaurants across the country, we’ve found that it’s often the quieter costs—the ones hiding in your vendor invoices, your POS settings, and the fifteen minutes your line cook clocks in before there’s anything to do—that don’t get the attention they deserve.

For a restaurant doing $2.5 million in annual revenue, the four hidden costs below can easily represent $40,000 to $80,000 in lost profit every year. That’s a kitchen renovation. That’s a marketing push.

Or think of it this way – saving $40,000 a year over the course of a 10 year lease invested at 7% rate of return would be over $550,000 in your pocket!

#1 — The True Interest Cost of Merchant Cash Advances

If you’re a regular reader, you might remember we covered MCAs in our Commonsense CPA: Top 3 Ways to Lose Money post last fall. We’re revisiting the topic because we keep seeing it—and the marketing around MCAs is designed to obscure just how bad the math really is (and woe is the business owner who clicked for a quote on a website and is now getting cold called for eternity).

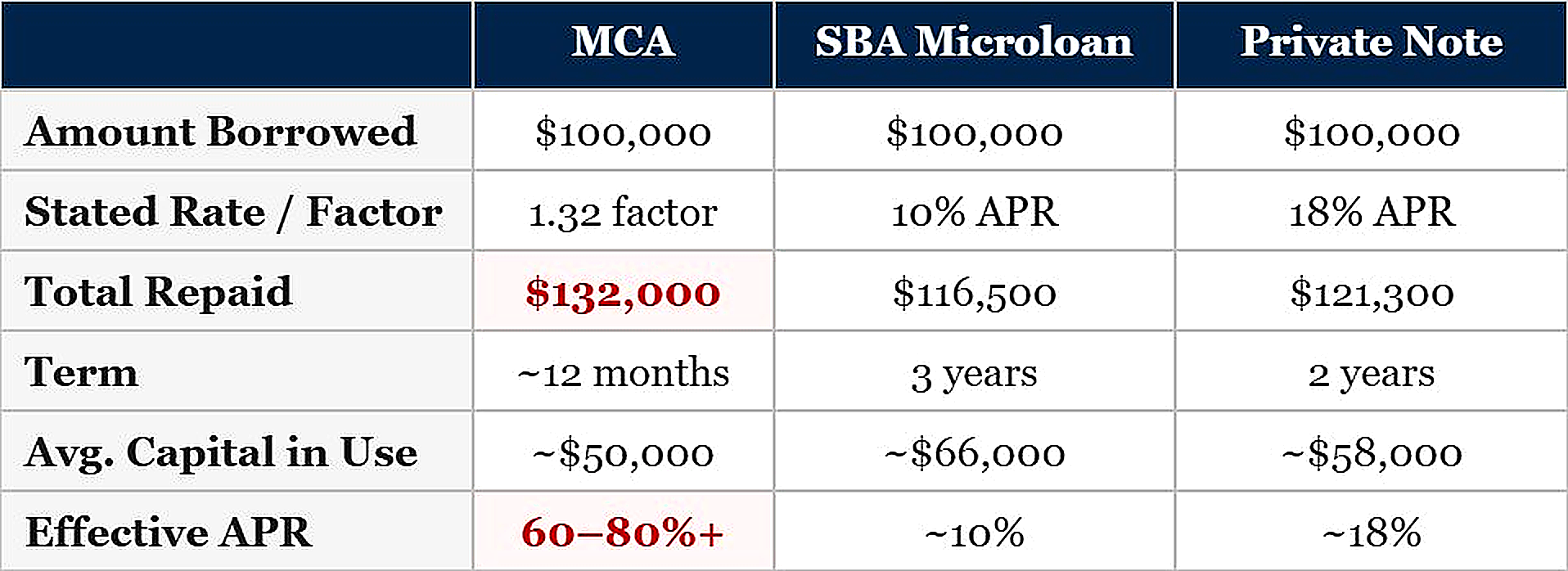

Here’s the pitch: borrow $100,000, repay $132,000 through daily deductions from your credit card receipts over 12 months. The $32,000 in fees looks like 32% interest. Expensive but manageable, right?

Wrong. That 32% is a flat fee on the original principal, but you’re paying it back daily. The first challenge is on your cash – you will be paying that money back immediately, not an ideal structure for a business in need of working capital.

This problem compounds – by month six you’ve returned half the borrowed amount, meaning you’re only using about $50,000 on average. Pay $32,000 to use $50,000 for a year and your effective APR lands north of 60–70%. We’ve seen structures exceeding 80%. And because MCA providers love offering a second advance before the first one is repaid, operators layer these on top of each other—paying interest on interest in a cycle that’s brutally hard to escape.

Here’s what a $100,000 MCA really looks like side by side with conventional financing:

Nick Wiseman, Founder of Little Sesame Hummus.

Same borrowed amount. Wildly different cost of capital.

For a $2.5M restaurant rolling advances twice a year, that’s $50,000–60,000 annually in financing costs—enough to eliminate the entire profit margin. Before you sign, call us. SBA microloans, a line of credit, even a private note at 15–20% is a fraction of the true MCA cost.

#2 — The 15-Minute Problem: Clock-In and Clock-Out Discipline

This one doesn’t feel like a big deal. Then you do the math.

If your staff clocks in 15 minutes early and clocks out 15 minutes late—and trust us, this is common—that’s 30 minutes of unproductive paid time per employee per shift. Across a team of 20 employees working 5 shifts a week, you’re looking at roughly 250 extra hours per month. At an average loaded rate of $18/hour, that’s $4,500 a month or $54,000 a year.

Even tightening by just 15 minutes total per shift translates to roughly 1.5 weeks of saved labor per employee annually—a 2–3 point reduction in your labor percentage. In this industry, that’s the difference between red and black.

The fix is operational discipline: set clear clock-in policies (no punching in more than five minutes before a scheduled start), configure your POS to flag early punches, review time reports weekly, and make it a management KPI. If your GM isn’t watching the clock, nobody is.

#3 — Vendor Pricing You Haven’t Reviewed Since Opening Day

When was the last time you ran a competitive bid on your major vendor contracts? If the answer is “when we opened” or “I don’t remember,” you’re almost certainly overpaying.

Vendor pricing is not static. Market conditions shift, contract terms expire, and your rep isn’t going to call you to lower your prices.

That’s your job.

In our accounts payable work, we routinely find clients paying 5–15% more than they should on staple categories like dairy, proteins, paper goods, and cleaning supplies. On a $2.5M restaurant spending $750,000–$850,000 a year on food and supplies, a 5% overpayment is $37,000–42,000 walking out the door.

Unlike labor optimization, this requires no operational changes—just a phone call and a willingness to compare quotes.

Conduct a formal vendor review at least twice a year around the time you do your quarterly budget review. Pull your top 10 spend categories, get competitive bids from at least two alternatives, and bring those numbers to your current vendors. Pricing gets “adjusted” fast when a rep realizes you’re shopping.

And don’t overlook linen service, pest control, or waste hauling—these creep up 3–5% annually with automatic renewals nobody is watching.

#4 — Selling at Dine-In Prices on Third-Party Delivery Apps

DoorDash, Uber Eats, and Grubhub charge commissions of 15–30% per order. If you’re running the same prices on those platforms that you charge in-house, you’re subsidizing every delivery order with your dine-in profits. Especially as Third-Party has gone from a marginal revenue stream to a revenue center representing a significant portion of sales.

Say delivery represents 15% of your $2.5M revenue—$375,000. At a blended 22% commission, you’re handing $82,500 to the platforms. Add 30% food cost ($112,500) and you’ve spent $195,000 against $375,000 in revenue—leaving $180,000 before a single dollar of labor, rent, or packaging.

The fix: mark up your delivery menu 15–20%. Most platforms allow separate pricing, and consumers expect it. That same delivery revenue repriced at an 18% markup becomes $442,500—an incremental $67,500 that drops almost entirely to your bottom line. That’s not a rounding error. That’s a line cook’s salary.

While you’re at it, curate a tighter delivery menu. Not every dish travels well. Treat third-party delivery as its own P&L—because it is one. Review your online prices in tandem with your in-house prices.

The Bottom Line

None of these costs show up on your P&L with a flashing red label. They accumulate quietly, month after month, and by the time you notice thin margins the damage is baked in.

The good news? Every one is fixable—and none require you to change your concept or raise dine-in prices.

They just require attention, discipline, and a willingness to look at the numbers. That’s what we do at Harmony. We’re in the books every week watching for exactly these profit leaks. If you're not already working with us and you'd like some help rooting out savings in your books, just get in touch below.